News published over the past two weeks have had a response to the high prices, particularly in the case of cereals and vegetable oils in all markets.

September 20, 2019

Strong rebound in global cereal prices

EM-ES-19-0064

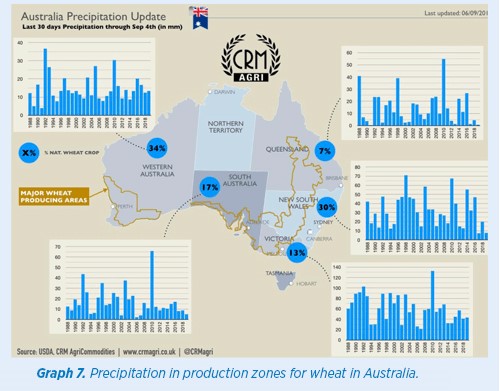

Regarding the fundamentals, only a few changes were observed and the most significant was the reduction of wheat production estimated for Australia, which we will comment on later.

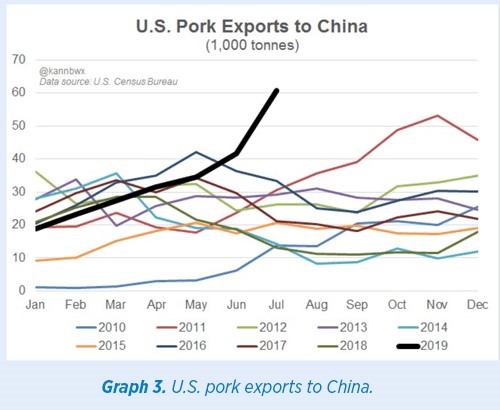

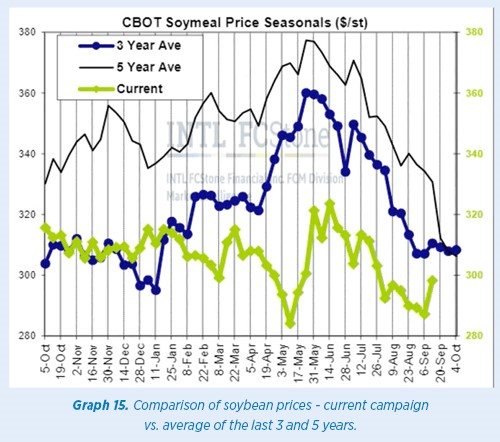

Regarding proteins, the market remains totally driven by the lower demand in China.

The production of pig feed is estimated to be 30% lower. This implies the reduction of 80/83 MMT that would be produced in the country, thereby reducing soybean meal consumption by around 20 MMT. We think that the U.S. Department of Agriculture (USDA) is not taking this into consideration in their demand balances.

Furthermore, they must be replacing animals in some farms, however producers are unsure about the occurrence of new contaminations and, due to this, some may decide to invest in other livestock species. We will see in the future what decisions are taken.

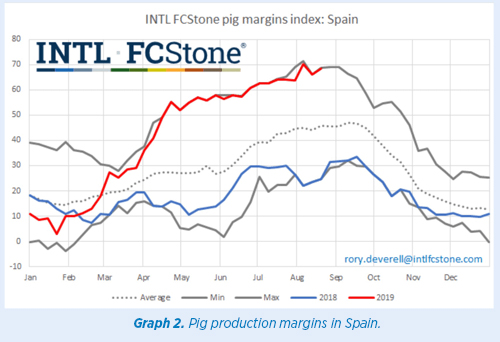

At the moment, pork-producing countries are delighted with the profit margins provided by the business in the current period.

Cereals

Corn

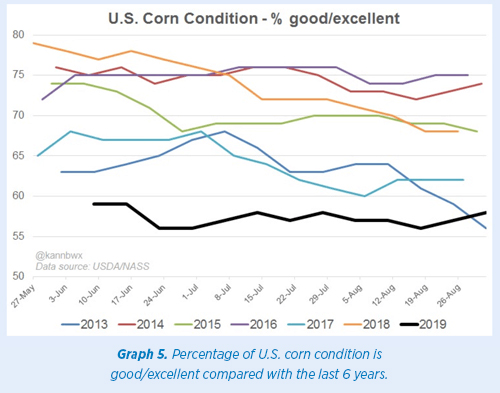

Weather forecasts for the next weeks in U.S. production areas are favorable, with proper temperatures and no risk of early frosts. Consequently, global production estimate continues to be good, despite the cutting back in the U.S.

The percentage of Good/Excellent condition is 55%. This is obviously below the historical levels after the known delay in sowing, but maintains the stocks with volumes that don’t allow for much pressure on prices.

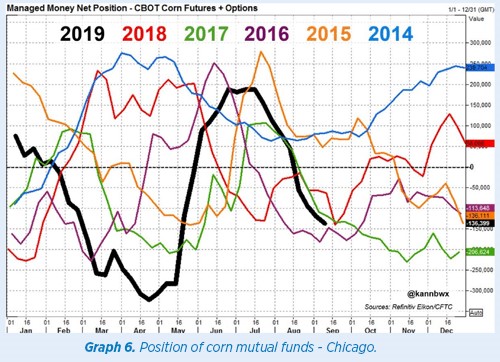

The funds continue to be sold, approaching 165,000 contracts.

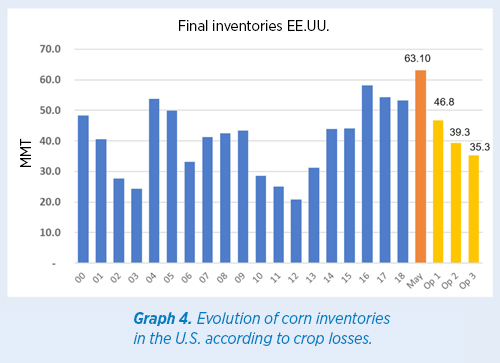

The major risk for price evolution regarding the global final stock expected for corn would be the fact that 65% of the total amount is located in China.

Wheat

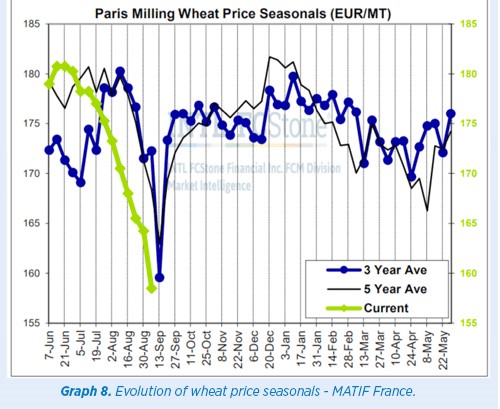

The world wheat balance is the “healthiest” compared with other grains, however as a relative value it is the product that has maintained the highest prices.

The market has registered an upturn between 3 and 4 €/MT in all positions, mainly due to the cut in global estimates as below:

![]()

![]()

As the global demand has also been cut in approximately 1.9 MMT, the impact on the safety stocks is low.

Perhaps the major condition for price increases has been caused by the seasonality. The northern hemisphere is finalizing the most decisive moment of crops, and we are now entering a period where the stored grains have 10 months to be commercialized.

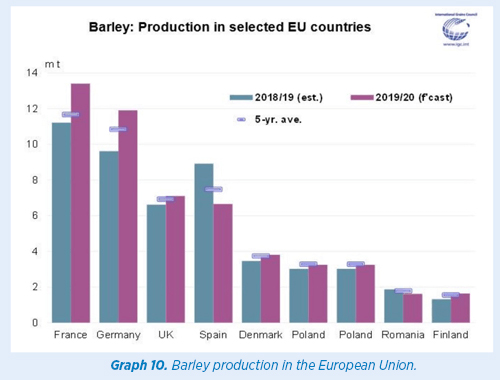

Barley

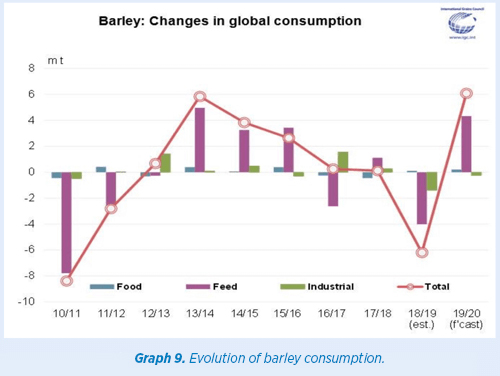

Overall, global barley harvests have recovered in terms of volume, as we can see in the graphs below.

However, the rebound of wheat and corn international markets, as well as the replacement of imported barley for November and December – which is not easy to get for far below 180 €/MT (warehouse-port) – led to a price rebound of around 2/3 €/MT in the inland areas last week, in all origins.

Proteins

China has purchased some products from the U.S. thanks to the good intentions between countries, which have allowed to postpone the tariff implementations announced from October 1.

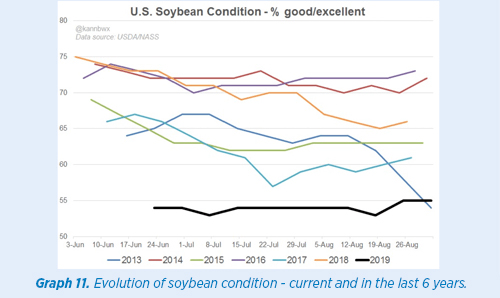

Currently, the condition of the U.S. crops remains unchanged, as what happens with the corn, that shows low production but without any climate threat that could negatively affect crop development in the next two weeks.

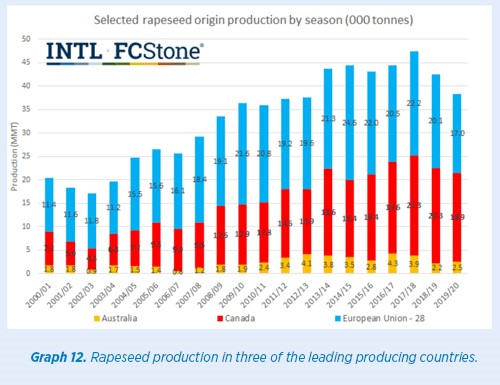

In regard to rapessed, global production has been decreasing for two years and, consequently, the nutritional competitiveness of rapeseed meal is being reduced when compared with soybean meal.

Vegetable oils

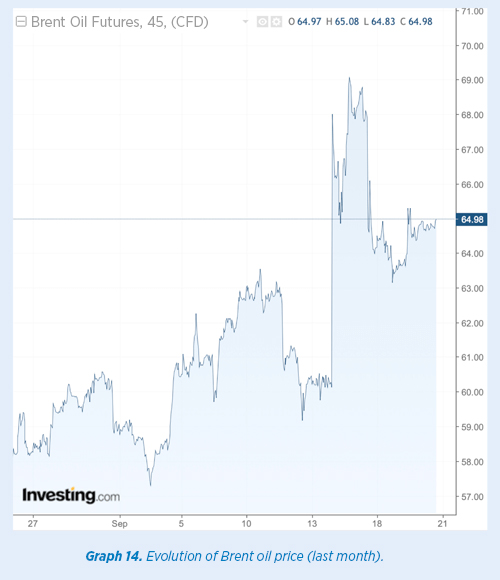

All vegetable oils have been dragged behind the rise in oil prices after the attack on the refinery in Saudi Arabia.

As we can see, the parallel of the curves (Brent Futures Curve and soybean oil) in Chicago confirms this.

Price forecast and predictions OCTOBER 2019

![]()

In the inland areas, with production in Duero region about to start, levels of 175 €/MT (origin) are offered in León for the old campaign, while we have 173/174 €/MT (exit) for the new campaign until January.

![]()

![]()

![]()

The large mainland ports still maintain the supply at around 175 €/MT (origin) for available goods.

This process of price increase is limited, particularly while corn trends remain unchanged.

![]()

![]()

![]()

The domestic extraction companies mainly produce low protein contents.

![]()

Regarding the other fibers, there will be no major changes until October.

Sources: U.S. Department of Agriculture, FC Stone, International Grains Council, Reuters, AESTIVUM, CRM Agri, Investing.com, CME Group, Agritel, and Eurotrade Agrícola.

EM-ES-19-0064

Elanco and the diagonal bar logo are trademarks of Elanco or its affiliates © 2019 Elanco Animal Health, Inc. or its affiliates.