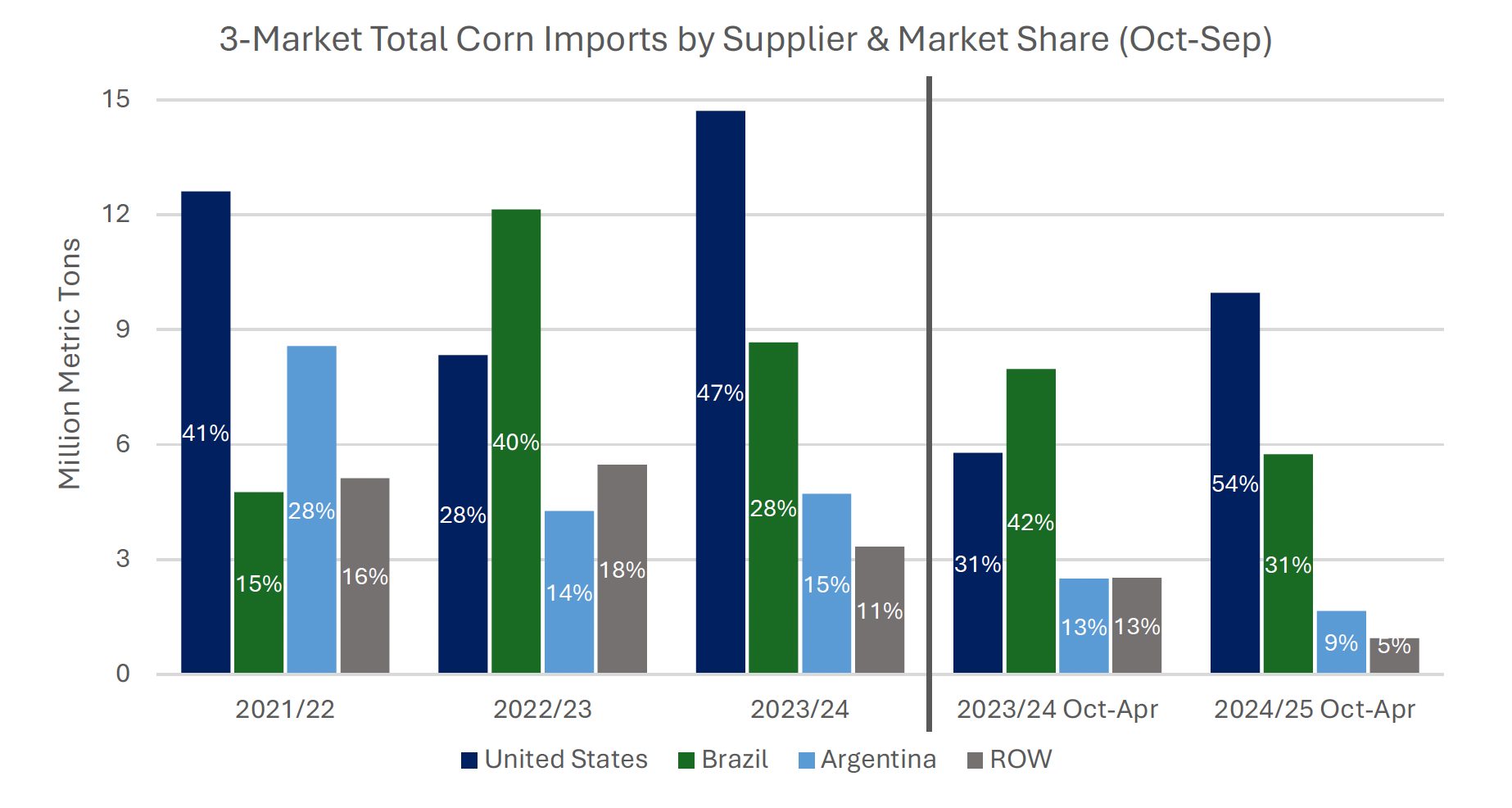

In the first 7 months of 2024/25 (October-September), Japan, South Korea, and Taiwan imported 10 million tons of US corn, a large gain from the 5.8 million tons during the same period last year, according to a report by USDA Foreign Agricultural Service .

US share of corn imports in these three markets jumped from 31% to 54% year-on-year. With 5 months left in the marketing year, US corn exports are likely to remain competitive in all three markets due to plentiful US supplies, lower exportable supplies from South America, and favorable exchange rates.

Throughout 2024/25 (October-September), US corn exports have remained strongly competitive with South American origins due to abundant supply and competitive prices, with US total supply expected to be the fourth highest on record following consecutive years of strong production.

With plentiful supply, export bids for US corn have been lower than those for Brazil corn since October 2024 and lower than Argentina corn for most of the year. Availability of Brazil’s 2024 safrinha crop has been constrained by increased domestic demand for animal feed and ethanol production, while Argentina has a smaller crop.

Japan, Korea, and Taiwan are highly sensitive to prices due to their significant dependence on imported inputs for feed.

- 🇹🇼 In Taiwan, the government eliminated the 5% business tax on corn and soybean imports in 2022 to help stabilize feed prices. This policy has been renewed multiple times and is currently scheduled to last through September 30, 2025.

- 🇰🇷 In Korea, price influences the choice between importing more corn or wheat, as both serve as alternative feedstocks for compound feed production.

- 🇯🇵 Japan mainly imports corn from the United States and Brazil, switching suppliers based on price.