Feed wheat use is falling in key Asian markets, according to the USDA Foreign Agricultural Service’s Grain: World Market and Trade report for August 2025.

Global wheat consumption is revised downward, driven by reduced feed and residual use in China, Indonesia, and the Philippines. These declines more than offset increased feed use in the EU.

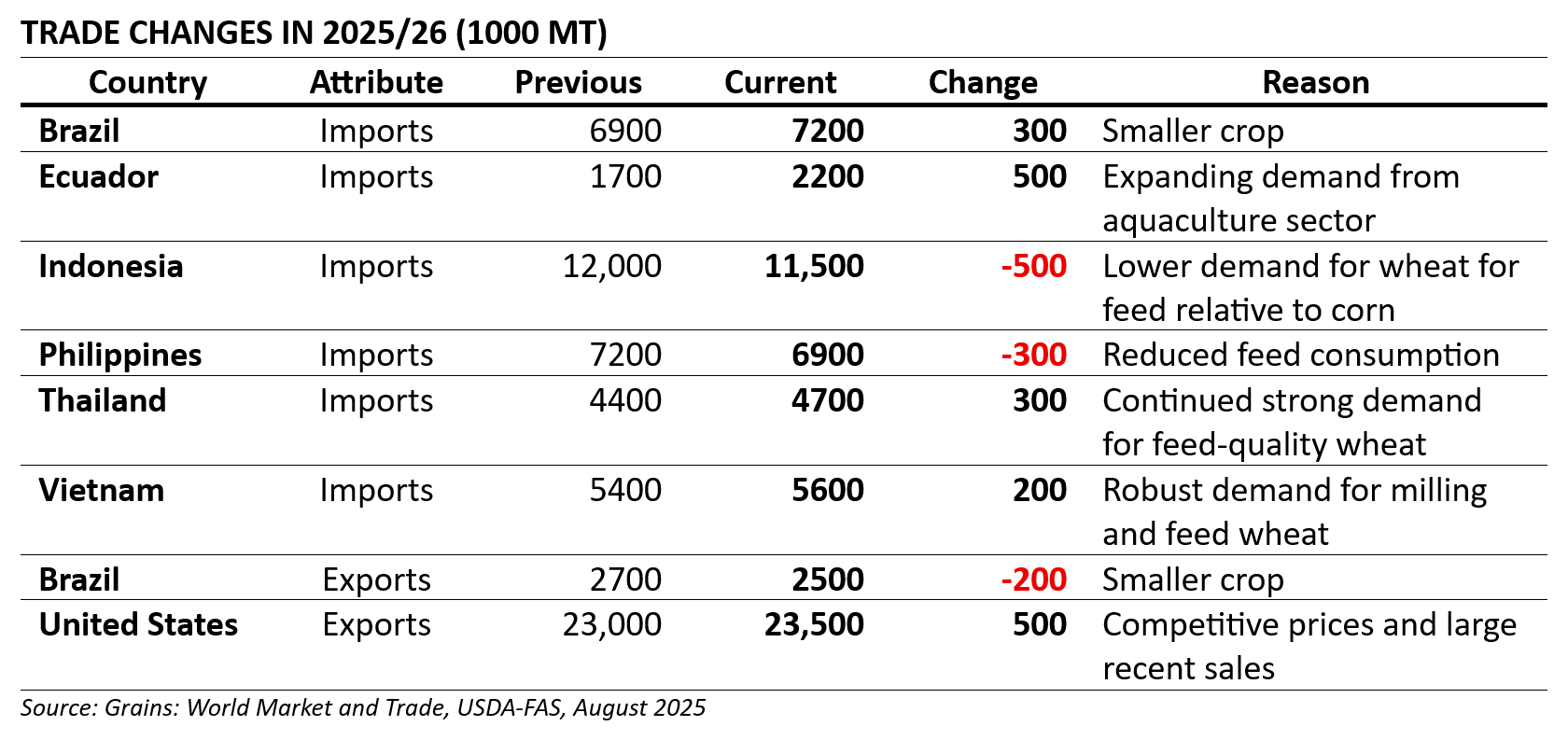

Production is also lower this month, with cuts in China, Brazil, and Argentina partially balanced by gains in the EU.

Global ending stocks are down, led by reductions in Ukraine and the US. Despite lower consumption, global trade is revised upward, with rising imports from Ecuador, Brazil, Thailand, and Vietnam.

US exports are also increased, supported by competitive pricing. The US season-average farm price is forecast 10 cents lower, now at USD 5.30/bushel.

Price movements: Mixed signals for buyers

US market:

- ✅ Hard Red Spring fell USD 22/ton to USD 252 due to global supply pressure, especially from Canada.

- ✅ Soft Red Winter dropped USD 1/ton to USD 220 as harvest nears completion.

- ✅ Hard Red Winter rose USD 2/ton to USD 235 on strong export demand.

- ✅ Soft White Winter remained unchanged at USD 241/ton.

Global market:

- ✅ Canadian wheat quotes dropped USD 26/ton with improved growing conditions, although prices remain highest among exporters.

- ✅ Australian quotes fell USD 7/ton following beneficial rains.

- ✅ EU quotes rose USD 7/ton amid cautious farmer selling.

- ✅ Russian quotes increased USD 11/ton as harvest progress lagged.

- ✅ Argentina rose USD 3/ton with planting now complete.

- ✅ US prices rose USD 2/ton and are currently among the most competitive globally.

For feed formulators and buyers, the report highlights shifting regional demand and pricing, reinforcing the need for agile sourcing and market monitoring.