25 May 2026

25 May 2026

In a cooperative office outside Bratislava early this year, a Slovak dairy official told his government something that would have been hard to say aloud two years ago: farmers in his region were losing ten euro cents (around 11 US cents) on every kilogram of milk they produced. Not on a bad month. Every month. And the number was still moving in the wrong direction.

Slovakia was not alone. Hungary, Bulgaria, and Italy stood with it at the EU Council of Agriculture in March 2026, all saying the same thing: European dairy farming is running at a structural loss, and without intervention, the damage will compound.

That crisis is now reaching Asia – through ingredient prices, supply chain shifts, and a fundamental change in who supplies what to whom.

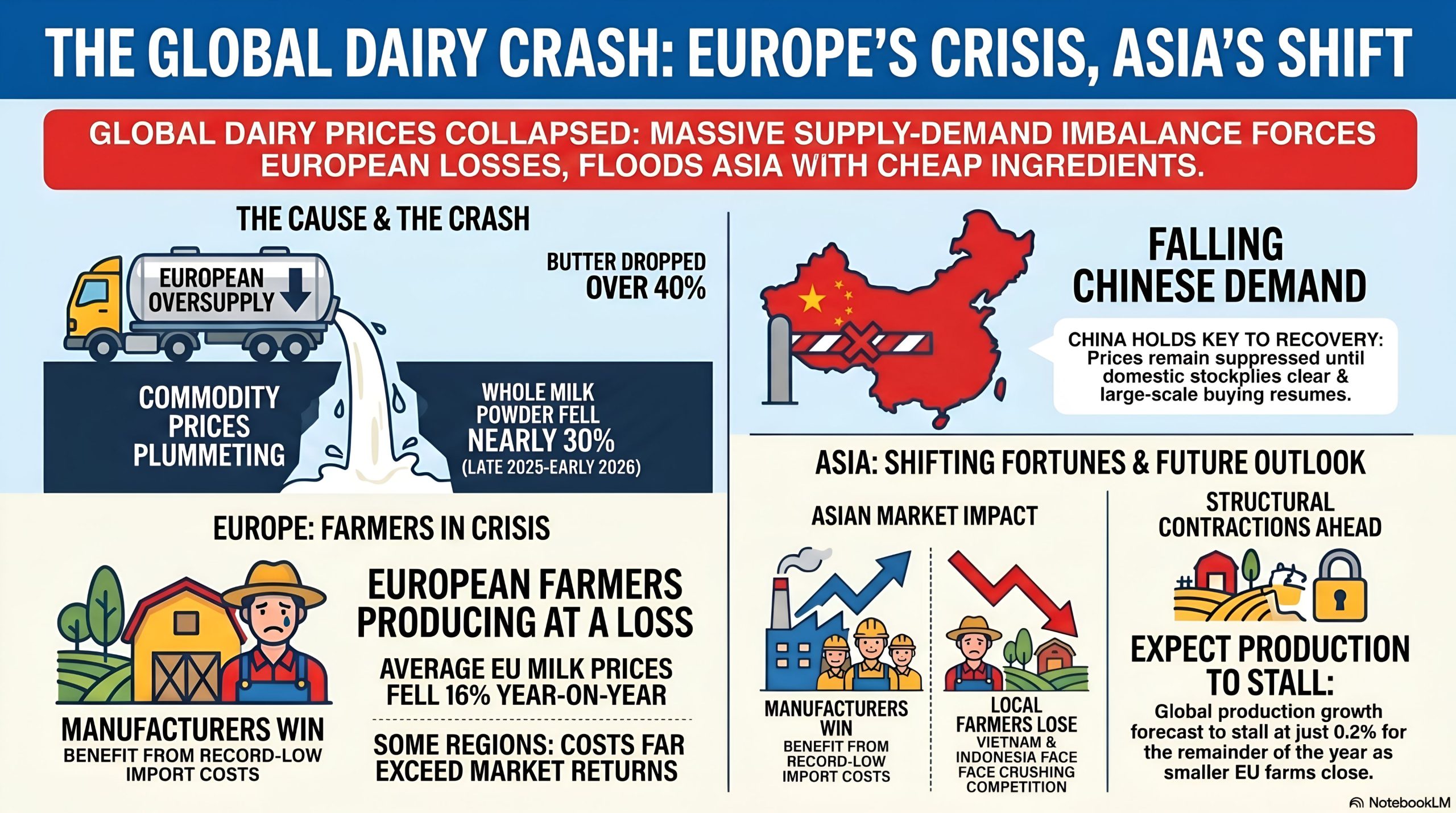

European dairy expanded steadily through 2024 and into 2025, driven by low feed costs. Herds grew, yields rose, and milk output surged. On its own, manageable. The problem was timing. The US, New Zealand, and South America expanded simultaneously, flooding the market.

European dairy expanded steadily through 2024 and into 2025, encouraged by low feed costs. More cows, higher output per animal, more milk. On its own, manageable. The problem was that every other major dairy region did the same thing at the same time. The US grew its herd to its largest in decades. New Zealand and South American producers expanded too. A market that depends on at least one region pulling back got no such relief.

Demand softened simultaneously. China – the buyer that for years set the floor under global whole milk powder and butter prices – reduced purchases sharply. Domestic stockpiles were full, the economy was slowing, and Chinese importers stepped back. European consumers, still feeling the weight of years of inflation, moved toward cheaper options. Processors found themselves holding more milk than the market wanted at any price that covered costs.

Butter prices dropped over 40% between September 2025 and February 2026. Whole milk powder fell nearly 30%. The FAO dairy price index recorded eight consecutive monthly declines. The Global Dairy Trade auction fell nine times in a row before a partial recovery, then slipped again in April.

Farmgate milk prices across the EU have fallen roughly 16% year-on-year. The EU average in January 2026 sat at USD 49.65 per 100 kilograms – down 6% from December alone. In some Italian spot markets, prices hit USD 22.85 per 100 kilograms in early 2026 – a figure that covers neither feed nor labour for most producers.

Production costs never adjusted to match. Fuel, labour, and regulatory compliance remain elevated from the inflation cycle of 2022–23. Farming milk is now a loss-making activity for a significant share of European producers.

The European Parliament has drawn comparisons to the 2016 dairy crisis and called for a voluntary production reduction scheme. Regardless of whether that activates, structural change is already underway. Smaller farms are closing or merging. EU milk production is forecast to contract for a second consecutive year. Processors are pivoting away from commodity butter and milk powder – historically the products most exported to Asia – toward cheese, whey, and high-protein lines where margins hold better.

The immediate effect for Asian food manufacturers is straightforward: imported dairy ingredients are cheaper than they have been in years. Butter, whole milk powder, skimmed milk powder, whey – all repriced significantly downward. For bakeries, infant formula producers, confectionery manufacturers, and dairy processors across Southeast Asia and the Middle East, current import prices represent a meaningful reduction in input costs.

The question is how long it holds, and whether European supply remains reliable as farm consolidation and production contraction reshape EU export capacity.

For domestic dairy producers in Vietnam, Indonesia, and Thailand — markets that have spent years building local production – the picture is less comfortable. Cheap imported milk powder undercuts locally produced alternatives. Governments that have invested in domestic dairy development are watching those investments face serious competitive pressure.

China’s role is distinct. It contributed to the oversupply by reducing purchases, and it will define the recovery. Chinese buyers will return – the only question is timing, and that depends on domestic economic conditions, stockpile drawdown, and currency movements.

India produces more milk than any country on earth – over 230 million tonnes annually, close to a quarter of global output. It exports almost none of it. The crisis in Bavaria or Bratislava registers only faintly in Anand or Amritsar.

The Indian dairy system feeds India first. Cooperatives like Amul stabilise procurement prices, absorb seasonal surplus, and keep the supply chain connected from village collection to urban retail. Through repeated global price cycles, that model has proven resilient.

Domestic pressures in 2026 are real but different in character. A near-25% surge in production during the 2024–25 flush season created a temporary surplus. Procurement costs have since risen while retail prices held steady after a GST cut. Bihar and Andhra Pradesh have already seen farmgate increases of one to one-and-a-half rupees per litre, with more likely before year end.

India has the production base. Whether it can convert that into competitive export volumes — in cheese, lactose, and nutritional dairy ingredients – is the real test of the next few years. The markets that are still growing their dairy consumption -Southeast Asia, the Middle East, Africa – sit closer to India than to Europe or New Zealand. The processing depth and export-grade consistency needed to reach them is coming, but not yet there.

EU herd contraction will gradually withdraw supply through the second half of 2026. Global milk production growth is forecast to slow from 2.6% in 2025 to around 0.2% this year. Both point toward some price recovery – but the pace depends heavily on China.

When Chinese buying resumes at scale, the surplus will clear. The uncertainty is the timeline. For Asia’s dairy industry – processors, importers, domestic producers, and ingredient buyers — that wait looks different depending on which side of the supply chain you sit on. Some will use the interval well. Others will find it has already decided things for them.

Subscribe now to the technical magazine of animal nutrition

AUTHORS

Consistency in Soybean Meal Drives Performance and Sustainability

Anna Cotcho

Kolin Plus FC: greener choline nutrition for poultry

Middle East conflicts disrupt global feed markets

Edgar Oviedo

Optimizing nutrition for dairy goat and sheep productivity in Cyprus

Carolina Kyriacou

pHix-up improves rumen stability in dairy cows

Subacute ruminal acidosis

Net energy and growth: keys to better prediction in swine production

Gabriela Martínez

How starch structure & protein reduction shape gut health in weaned pigs

Diana Luise

Astaxanthin supplementation in aquaculture

Babatunde Saliu

What is intestinal health?

Marcos Rostagno

Calcium, phosphorus, and phytase optimization in broiler diets

Anna Cotcho